So far in 2018, we at FactRight have been kept very busy reviewing DST offerings for our clients, including deals from new sponsors entering the market. Recent tax reform spared section 1031 exchanges for interests in real estate, and the industry breathed a sigh of relief, as it expects demand for syndicated deals will continue to grow. Our friends at Mountain Dell Consulting report that 29 sponsors raised more than $1.9 billion in aggregate equity in 2017, making it the most active year for syndicated 1031 offerings since 2007 (during which $2.8 billion was raised by 64 sponsors). The sentiment appears to be that the growth we’ve seen in the overall market since 2011 will continue into the foreseeable future.

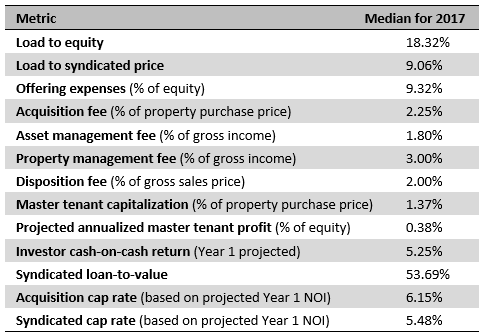

We’ve recently enhanced the content and format of our due diligence reports on DSTs to deliver more value-add assessment for our clients. We believe these improvements put offering terms and features into clearer context. For instance, we compare fees and expenses in the specific offering under review to customary ranges and medians gleaned from our extensive DST offering database. I thought you might be interested to see the medians for some of the metrics we track from the offerings we reviewed in 2017 (in the table below). You’ll find more of this kind of data in our reports.

Of course, these data points should not be viewed in isolation. Fees in a specific deal should be considered on not only an individual, but also a global basis, especially as sponsors can pull different fee “levers” in an offering. Other metrics need to be weighed against caveats. Appropriate questions to ask when reviewing a specific offering include:

- If overall upfront load has decreased from previous offerings by this sponsor, is the sponsor stealthily raising ongoing fees?

- What is the total ongoing compensation to the sponsor and its affiliates, including property management, asset management, and other fees, as well as projected master tenant profit? (For instance, a deal may have a relatively low property management fee, but the asset management fee may change every year to engineer a round cash flow number to investors. You need to put that asset management fee into the same context as the property management fee—as a function of gross income—to see a fuller picture.)

- What kind of fee considerations attend the type of asset class, and the related level of underwriting difficulty and management intensity? Some metrics, such as acquisition and management fees, should be assessed against other deals of that asset class only (which we also track).

- Are there reasons why some metrics may be not customary? For instance, small equity raises will make loads-to-equity look high, and deals with no debt will have identical load-to-equity and -syndicated measures. Relatively high (or low) LTVs can also skew metrics.

- While DSTs have to be structured carefully to avoid characterization as a partnership for 1031 purposes, there are ways for sponsors subordinate some of their compensation to investor return. Is the disposition fee contingent on full return of investor capital? Also, understand how the structure of the master lease dictates how property profit flows between investors and the master tenant.

In the end, the critical question is: assuming DST investors can receive their tax deferral benefits, is the return reasonable for the risk the investors will take on? We hope data like this can help you answer that question more confidently.